Hello Friends, and welcome to Split Second! If you are new here, click on the Subscribe button below to keep up with all new posts. If you want to read old posts, check out my archive here!

Had an absolute pleasure writing this piece alongside Teddy Feldmann, a rockstar in the making in the mining industry. Give him a follow on X @teddyfeld and his excellent Substack “Its Time to Mine”. This is the first piece of a two part series on the nuclear fuel cycle that we worked on together. This piece will focus on the market analysis, while the second will focus on the technical components of the fuel cycle. Special shoutout to Adam Rodman from Segra Capital who provided very useful information for this piece. Also the team at Goehring & Rozencwajg. Savvy researchers and smart guys.

2023 has been a banner year for the nuclear energy industry. The iron laws of physics have prevailed yet again, and a series of fortuitous tailwinds have once again pressed the magic of atomic energy into the public spotlight. For those who oppose Malthusian theories, the nuclear renaissance has given renewed optimism for a world of energy abundance. Given the year that the industry has had, it's important to understand the dynamics in the fuel market and how it may shape things going forward.

(For those less familiar with nuclear energy’s history and value propositions, I highly recommend first reading this primer by Julia DeWahl. An exceptional piece)

One of the key assumptions in this writing is that the demand for nuclear energy is increasing. While the possibility of long tail risk always exists in this market, for the sake of this piece, we will recognize many of the serious tailwinds that are pushing demand to unprecedented heights.

Why is demand for uranium Increasing?

Net Zero Goals

Government officials throughout the globe have declared a war on climate change, and have drawn their lines in the sand to hold themselves and their constituents accountable for decarbonization. A variety of benchmarks have been set for 2030 and 2040, including Joe Biden’s pledge to cut emissions by 35-43% by 2030. This comes despite the fact that hydrocarbons had a record year in 2022, where they accounted for 81% of domestic primary energy production. Not to mention new highs are expected in 2023.

What once was up for debate in the eyes of few, is now no longer worth a discussion. Current net zero goals are impossible without scaling nuclear energy. Full stop. Ask any climate scientist to model out possible scenarios and they will also come to this conclusion. Luckily for all, this is neither hypothesis or theory, as our friends across the pond in France have confirmed that nuclear energy can indeed replace hydrocarbons to fulfill ever increasing base load. demand. And in remarkable fashion.

France’s successful transition to nuclear energy. Seeing is believing.

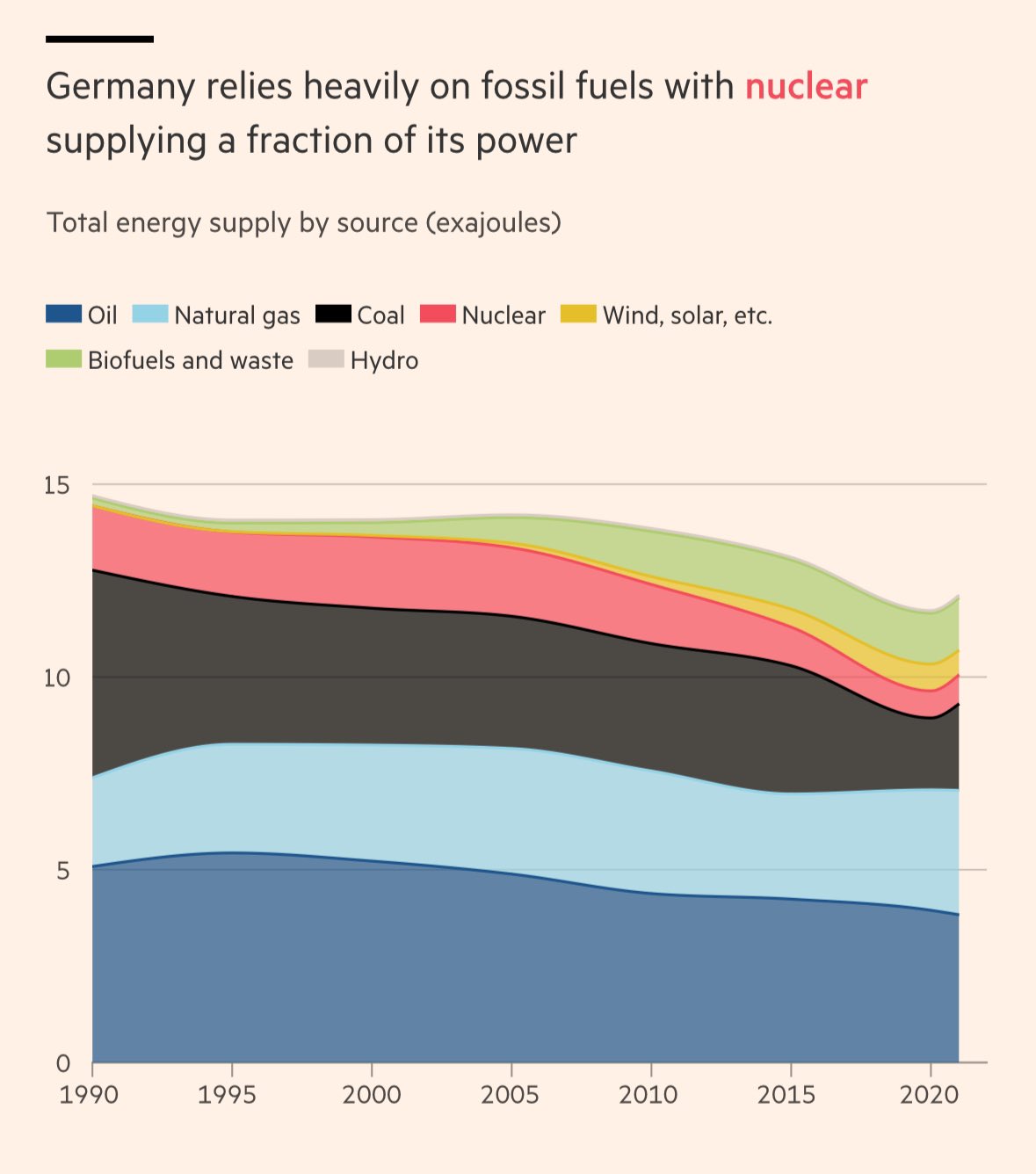

Germany on the other hand, who have now fully phased out nuclear power, seem unserious about the growing threats of climate change. Germany saw a 5% increase in electricity generated from coal from 2021 to 2022, and remain one of the largest global consumers of lignite, which happens to be the dirtiest form of coal.

Germany’s total energy supply by source

The urgency of the matter will force the hand of many nations around the world to ensure that nuclear energy is a core tenet of a decarbonization strategy. Here is a quick snapshot of who is building what as of 2023.

Nuclear reactors under construction by country. China playing chess, per usual. USA twiddling thumbs.

Geopolitical Uncertainty and the Changing World Order

The Russian invasion of Ukraine in 2022, the currently devolving situation in the Middle East, and a looming invasion of Taiwan by China underpin a greater shift in the stability of world order (great piece by Noah Smith on this topic). One of the direct effects of the Russian invasion were immediate concerns for energy security across Europe. Those that were reliant on cheap Russian natural gas pre-Nordstream pipeline explosion became some of the most competitive buyers of liquified natural gas (LNG) overnight, sending ripple effects across the world.

Countries like Pakistan ended up getting the short end of the stick as millions across the nation became subject to rolling blackouts due to energy shortages. They could not afford the massive increase in spot prices for LNG and were forced to turn elsewhere. The nation has now pledged to quadruple coal-fired power as they reduce reliance on natural gas imports. A perfect example of how unsound energy policy can disproportionately affect those in emerging markets.

Energy is life, and given the risk a destabilizing geopolitical landscape poses to supply chains, many began to introspect critically about their respective domestic situations. Energy security has again been deemed national security.

The back half of 2022 saw a rapid scramble for natural gas and coal, as securing domestic access to energy emerged as a way to ward off larger risks. When millions were cut off from cheap Russian gas, there was a mad dash to secure ancillary resources. As nicely summarized by a partner at London law firm Vinson & Elkins LLP, “Right now the sentiment is that more coal is better than more Russia.”

The murky waters and changing tides of the geopolitical landscape bodes extremely well for the future of nuclear. Holding the throne as the most dense form of primary energy in the market, governments with understandings of the physics of energy density (primarily China amongst a few others) now represent a total of 300 reactors in proposal phasings, complimenting the 440 in operation today. A massive increase. An obvious, secular trend of increasing demand for nuclear fuel.

Other Bullish Trends for Demand Increase

Here is a rapid fire list of other important happenings:

Sam Altman and Bill Gates, titans of Silicon Valley, have indicated their support for nuclear energy via Oklo and TerraPower

Rapid rise in artificial intelligence (energy intensive) has led Microsoft to start looking at implementing a small modular reactor strategy

Advances in reactor design

Americans' support for nuclear energy is highest in a decade

More than 20 countries from 4 continents pledge to triple nuclear energy capacity by 2050 at COP28

What are the unique market dynamics in the nuclear fuel cycle?

Given the information as described above, it can be easy to see through rose-tinted glasses when thinking about what the future holds for this industry. However, the nuclear fuel cycle is complex and opaque, with long lead times and lack of primary research available. Now that the importance of nuclear has emerged center stage as a more consensus viewpoint, it is more important than ever to understand the market dynamics in this value chain.

Based on all the momentum and commitments to build out capacity, demand for fuel can be assumed as a given. Unlike crude oil and many other commodities, forecasting demand in uranium markets is relatively straightforward. Uranium has one downstream use case, a significant difference than crude which is refined into an array of different products (diesel, gasoline, petrochemicals, lubricants, etc). This lack of versatility makes it a simpler calculation when modeling the demand side of the equation.

Also differing from other commodities, uranium cost curves don't perfectly marry each other and supply and demand equations are not perfectly efficient. There are a few reasons for this, with a significant one being long lead times. If a utility buyer is low on fuel, they would need to be buying uranium at minimum 2 years ahead so that it can be ready for use in a timely manner. The fuel cycle takes about 18-24 months and contracting for deliveries occurs over a 5-10 year period, leading buyers to run relatively high inventory.

Another unique characteristic of the nuclear fuel markets is that buyers at utilities are not price sensitive. There are a few factors that play into this. One notable one is fuel costs for nuclear plants represent a small percentage of total costs. Non-commodity expenditures far exceed fuel costs and ultimately drive the economics of the industry, leaving little incentive to be a smart buyer. The World Nuclear Association underscores a notable cost differential in power generation: fuel expenses for nuclear power plants are markedly lower compared to those for gas combined-cycle plants, often just a fraction—about one-fifth to one-fourth—of total operational costs. In stark contrast, for coal and gas plants, feedstock costs can account for a substantial 80% of their operating expenses. This significant difference means price fluctuations have a much greater impact on coal and gas operations, making price sensitivity a key concern for traders in these sectors, unlike the more stable cost structure in nuclear power.

Lastly, the lack of information makes it a complex read for those on the outside looking in. Given the unpopularity of uranium in the 2010’s, the infrastructure around trading the fuel cycle is bare relative to others. There are very few flow traders and much of the primary research has to be done through phone calls to ascertain who has tonnage. There is no volume quoted on spot prices along with very little intraday price changes, leaving very little data left for those still interested. Ultimately, the dearth of information is completely irrelevant to end users, but these factors are important to note when trying to understand market dynamics of the fuel cycle nonetheless.

What does the market look like today?

The nuclear fuel market has been in equilibrium or surplus for the last several decades. In the early 1970’s commercial nuclear power started gaining serious traction. Installed capacity grew tenfold every decade from 1GW in 1960 to 100 GW by 1980. Despite this adoption, mine supply grew faster than reactor demand, leaving the market in a state of surplus to the tune of ~400mm lbs of U3O8 aka yellowcake.

Changes in Commercial Uranium Inventory from Goehring & Rozencwajg

Some may note that the industry was technically in a deficit starting in the late 80’s through Fukushima (2011), however, secondary sources of uranium were able to fill any shortfalls that existed. The most notable source being the “Megatons for Megawatts” program between the U.S. and Russia where bomb-grade uranium was converted and fabricated into lower-enrichment grade fuel. Fuel recycling also gained popularity during this time period, especially in France, and contributed to the “secondary sources” as reflected in the chart above.

After decades of being in equilibrium or surplus, things began to change when Cameco and Kazatomprom, the duopoly in uranium mining, began to limit production around 2017. This can be looked at as the beginning of what seems to be a new era of structural deficit for the industry. Reactor demand is set to grow 28% by 2030 going from 188mm lbs to 240mm lbs, dwarfing the projections on growth of primary production, which currently stands at 140mm lbs.

This spread is being reflected in the rapid rise in the spot prices of uranium in 2023, with a nearly 82% increase year to date, reaching the highest levels in nearly 15 years. There still remains plenty of optimism that the price has continued upside as mining production will take lengthy periods of time to come online and help ease pressure on the market. Not to mention there are already current struggles unfolding as Cameco indicated in September that they had downgraded production forecasts for the year, leading to potential purchases of uranium from others to fulfill contracts in Q4 of 2023. Fellow production giant Kazatomprom says shortages of sulfuric acid are creating issues in the milling process, posing a risk to production.

Nonetheless, the uranium markets are seemingly one of the tightest of any commodity and are now attracting attention the industry has not seen in decades.

Arguably the most intriguing aspect of the market today is how large of a role geopolitics plays. As noted earlier, a transition from a unipolar to multipolar global order should bode well for nuclear, but there are other things to keep an eye on that can tighten the market to even greater levels than what some analysts are currently underwriting.

For example, in July of 2023 a military coup was attempted in Niger, immediately endangering production in a country that accounts for 5% of global supplies. French multinational Orano has indicated that everything is “under control”, but further instability in the Sahel poses a significant risk to a source of supply that accounts of 25% of the uranium used by the EU. The late Yevgeny Prighozin, leader of the Wagner mercenary group hailed the moment as a win for the people of Niger against their colonizers who are “trying to keep them in the state that Africa was in hundreds of years ago.” While Prigozhin’s death was ultimately due to his military clout producing an increasing threat internally to the Kremlin, his words regarding Niger help to shed light on how Russia as a country aims to benefit from further instability in the nuclear fuel cycle in Niger and around the world.

While not necessarily a uranium mining powerhouse, Russia, via state owned Rosatom, currently controls upwards of 40% of the market for uranium conversion and enrichment, two fundamental midstream stages of the fuel cycle that we will delve into deeper in the next piece. This is a clear strategic vulnerability for the United States and fellow allies, who still are heavily reliant on the services of Russian-backed entities. U.S. utilities are currently forking over approximately $1B per year to Russian-based entities.

Despite calls for reducing reliance on Russia’s stranglehold over the value chain, these are issues that are impossible to be solved overnight. As seen through the United State’s ineffective sanctions on Russian crude exports, where almost zero barrels of oil have been settled below the $60 price cap that was set by the U.S., acts of economic warfare may be ineffective and further push the uranium market into even tighter conditions. Interesting times, indeed.

2024 will prove to be another fascinating year for the nuclear industry and the fuel cycle that accompanies it. With so much unfolding across the globe, between geopolitical conflicts and a race to net-zero, the nuclear industry stands poised to serve as a battleground for energy security as well as moral and political high ground. The stakes remain as high as ever for the beauty that is atomic energy.